2026, China's photovoltaic industry inflection point. This turning point is not driven by a single factor, but the same frequency resonance of the three major changes in market size, business model and technology route. At the market size level, the industry has shifted from the rapid expansion of installed capacity to the stage of high-quality development. After hitting a record high of 316.6GW in 2025, the industry generally predicts that the installed capacity will fall back to 220-240GW in 2026, with a rational correction. At the business model level, the incremental photovoltaic project feed-in tariff has basically achieved market-oriented transactions, as of March 2026, more than 23 provinces and cities have completed the year's mechanism of electricity bidding, electricity market-oriented transactions have become the new normal. At the technical route level, efficient products represented by BC technology are taking advantage of the situation to rapidly increase their market share, gradually moving from the former "bonus items" to the "must option" that determines the success or failure of enterprises ".

Good winds rely on force. The 2026 government work report clearly put forward "in-depth rectification of the 'inner-roll' competition", and the Ministry of Industry and Information Technology defined this year as "the year of the governance of the photovoltaic industry". During the two sessions, a number of industry representatives around the "anti-roll" actively advice and suggestions, together to outline the photovoltaic industry from the "price war" to "value war" clear path. Behind this is the new requirements put forward by the state for the high-quality development of the photovoltaic industry, but also the common choice of manufacturing enterprises and power plant developers based on the comprehensive consideration of technical performance, cost-down path, market application, macro trends and patent ecology.

technical performance: double "moat" of efficiency and value

in the 51st TOP SOLAR MODULES list released by aiyangNews in March 2026, BC component continued to dominate the top two with an absolute advantage of 1% ahead of the third place. Since the release of the list in December 2021, BC products have always occupied the top spot, and there is no doubt about the technical leadership.

More importantly, the efficiency potential of BC technology is far from touching the ceiling. At present, TOPCon battery in a variety of technical support, laboratory efficiency has been close to 27%, approaching its theoretical limit, continue to improve the technical difficulty and capital investment will be exponential growth, economic concerns. The BC battery not only has the latest laboratory efficiency record of 27.8 percent, but also can continue to make breakthroughs by compatible with existing efficiency improvement technologies such as half-chip passivation, 0BB, and stacked gate, as well as optimizing cutting-edge processes such as back patterning and bipolar composite passivation. It is expected that the efficiency of BC mass production battery is expected to increase to 28.7 percent in the future, and the limit is close to the theoretical limit of 29.4 percent crystalline silicon, which has laid a solid scientific foundation for it to become the absolute mainstream of the future market.

However, the value of BC goes far beyond digital leadership and the actual economic benefits it brings to end users. Under the same land area, the installed capacity is about 6% higher than that of TOPCon components. Under the same installed capacity, land costs, BOS costs, operation and maintenance costs to obtain significant savings, superimposed on the single watt of excellent power generation capacity, for customers to create an estimated 8-20 points of value-added benefits. In the context of rising component prices and high development costs, this advantage has been significantly amplified. In addition, thanks to the inherent structural advantages, BC components can achieve higher power generation in high electricity price periods with low irradiation in the morning and evening, as well as in complex scenarios with shadow occlusion such as mountain and offshore photovoltaics, further enhancing the internal rate of return (IRR) throughout the life cycle of the project.

path to cost reduction: the "de-silvering" breakout cost curve has steeply declined

since 2025, the price of silver has risen by up to nearly 400 due to the influence of global economy, geopolitics and supply and demand relations, and has recently remained at a high level of 20000 yuan/kg, becoming the largest variable in the cost of photovoltaic modules. The cost of single-watt silver paste for conventional TOPCon components climbed to 0.15-0.20 yuan, while the amount of silver used for high-efficiency TOPCon products was about 30% higher than that of conventional products. The cost of single-watt silver paste even reached 0.20-0.26 yuan, seriously eroding corporate profits and causing the industry to "talk about silver change".

Faced with the challenge of skyrocketing silver prices, BC technology manufacturers have successfully opened up a clear path to cost reduction with a forward-looking layout. As early as 2024, a number of BC leading enterprises started the research and development of "silver reduction" and even "no silver" technology. At present, Aixu's copper electroplating, Longji's alloy slurry, GCL's new gate wire, and Zhonglai's aluminum-based silver technology have all made breakthroughs. These innovations not only effectively reduced the production cost of BC components, but also fundamentally weakened its dependence on the price fluctuations of commodities such as silver, and built a more resilient supply chain system.

market application: from "pioneer exploration" to "mainstream selection"

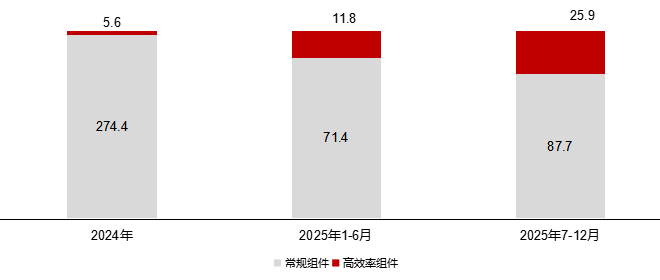

2024-2025 bidding component technology type (GW,%)

the bidding wind direction changes: since the second half of 2025, the total bidding volume of high-efficiency product bid sections including BC and HJT has reached 25.9GW, accounting for 24.1 percent. China Huaneng, China Huadian, China Three Gorges component collection, and a number of project tenders are divided according to the conversion efficiency of the bid section, the lower limit of high-efficiency component bid section is set to 23.8, the lowest proportion of high-efficiency bid section is 48%, to the central state-owned enterprises-based power station development enterprises to confirm the recognition of high-efficiency products. This change in the bidding model is a positive response to the "abandonment of the 'only low-priced bid.

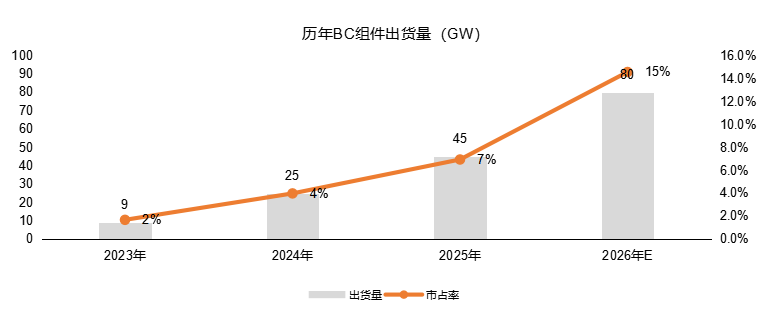

shipments blowout: by the third quarter of 2025, the cumulative shipments of BC components of Longji green energy and Aixu shares alone have exceeded 26GW. Among them, Longji shipped 14.5GW, accounting for about 24% of its total component shipments, is expected to increase the proportion of annual shipments to 25%-30%. As more manufacturers of BC products begin mass production shipments, total BC product shipments are expected to reach 45GW in 2025. The surge in shipments is directly reflected in the financial performance of the company-against the backdrop of widespread industry-wide losses in 2025, Longi and Aixu are on a positive trend in profitability and cash flow with the differentiated competitive advantage of BC products.

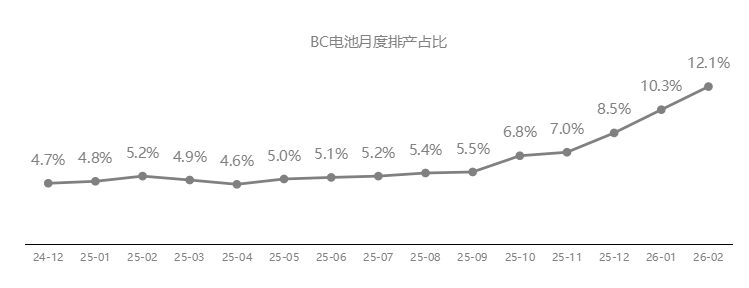

rapid expansion of production capacity: according to incomplete statistics, by the end of 2025, the global BC battery production capacity under construction and landing has reached 88GW, with an average monthly output of about 3.5GW and an operating rate of about 50%, it accounts for about 5.7 percent of battery production. Entering January-February 2026, the monthly output of BC batteries exceeded 4GW, the operating rate was close to 60%, and the proportion of battery production in the whole industry jumped from 5.7 to 10-12%. Under the background that P-type and even a large number of TOPCon production lines have stopped production due to overcapacity and the operating rate is less than 30%, BC technology continues to maintain a high operating rate and expand against the trend, fully demonstrating the strong market demand for efficient products. It is expected that by the end of 2026, the total capacity of BC batteries will increase to about 150GW, and the scale effect of the industry will be fully apparent.

Macro Policy: National Standards Lead, Local Projects Priority

Note: The final data is subject to the actual release version, the component power is calculated according to the conventional plate type (2382*1134mm)

during the two sessions, Gao Jifan's representative suggested "strict standards to lead and accelerate the clearance of backward production capacity", and Zhong Baoshen's representative also proposed "improving the national mandatory safety access standard for component products". Since 2025, national and local governments have issued a series of policies to translate these suggestions into reality.

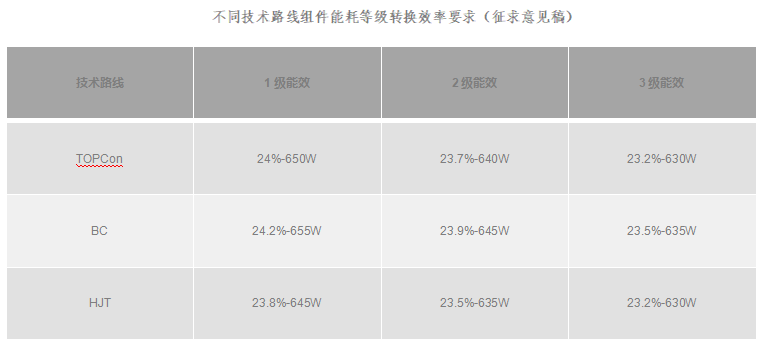

National standards establish energy efficiency thresholds: Recently, the State Administration of Market Supervision and Administration, the State Standardization Administration and the National Photovoltaic Quality Inspection Center (CPVT) jointly formulated the "Crystalline Silicon Photovoltaic Modules and Inverters Energy Efficiency Limits and Energy Efficiency Ratings". According to the draft, at the mass production level, only BC components can meet the level 1 energy efficiency standard (conversion efficiency ≥ 24.2%). The introduction of this standard will become one of the important technical basis for eliminating backward production capacity, supporting technological innovation and selecting efficient products.

local governments give priority to: in the development and construction of wind power and photovoltaic power generation projects in 2025, Shaanxi province clearly proposes to encourage the use of components with conversion efficiency of more than 24.2 percent for projects applying for the "photovoltaic leader plan. Shaoguan City, Guangdong Province, Guangnan County, Yunnan Province and other places have also issued documents, in the preferred configuration of distributed photovoltaic and ground power station projects, explicitly encourage or give priority to the use of advanced photovoltaic modules with conversion efficiency of 24% and above. The strong guidance of the policy has created a broader market space for the large-scale application of BC technology.

patent and industrial ecology: building a virtuous circle of "moat" and "circle of friends"

Gao Jifan's representative called for many times during the two sessions: "speed up the construction of photovoltaic patent pool and protect the hard-won commanding heights of global technology"; at the same time, it emphasizes "increasing the investigation and punishment of malicious infringement, trade secret theft and other acts". TOPCon technology has been deeply involved in patent disputes in recent years. In February this year, First Solar, an American photovoltaic manufacturer, once again sued a number of Chinese photovoltaic enterprises on the grounds of patent infringement, continuing its previous "337 investigation" of TOPCon technology patents. However, it is worth noting that in the second half of 2025, Longji Green Energy and Jingke Energy, Jingao Technology and Chint New Energy, including industry leaders, have reached patent settlements through cross-licensing of core patents. And explain three clear signals: first, the industry competition has shifted from low-cost internal volume to high-quality competition of technological innovation.

The patent moat is deep: BC technology covers the integrated innovation of the whole chain of silicon wafers, battery structure, laser patterning, metallization, etc., forming a more solid barrier to intellectual property rights and industrial synergy, not only protecting the interests of innovators, but also avoiding low-level price wars. As a pioneer of BC technology in China, Longji Green Energy and Aixu shares have built a deep patent moat. As of June 2025, Longi alone has 480 patents for BC battery components. In early 2025, TCL Central acquired Maxeon's BC battery and component patents other than the United States through an equity acquisition, while Maxeon's BC battery and component patents also built a global intellectual property barrier for it.

The industrial ecosystem is increasingly prosperous: More importantly, BC's "single spark" has become a "prairie fire". Since 2025, more than 22 head enterprises, such as TCL Central, Gaojing, GCL, Jingao, Tongwei, Tianhe, One, Zhonglai, etc., have cut into the BC track through new construction, technical transformation or release of new products. From Longji (70GW planning) and Aixu (25GW +) that have been mass-produced, to Xiexin, TCL Central, Gaojing and Huayao that have been partially mass-produced, to Jingke, Jingao, Tianhe, Tongwei, Jietai and Yingfa in the pilot and technical reserve stages, a BC technical camp covering the whole industrial chain has become spectacular.

At the same time, the BC ecosystem is becoming more and more perfect. A large number of local equipment and material suppliers, such as Dier, Shengxiong and Haimu at the laser equipment end, Jiejia Chuangwei, Microconductive Nanometer and Laplace at the coating equipment end, Guangxin Material and Foster at the material end, Otway and Pilot Intelligence at the series welding equipment end, are working closely with battery component enterprises to jointly promote the maturity and cost reduction of BC industrial chain. This benign interaction of localization substitution provides a powerful boost to the continuous iteration and large-scale development of BC technology.

why BC technology has become a "must" in the year of governance

in March 2026, Wang shijiang, deputy director of the electronic information department of the Ministry of industry and information technology, clearly pointed out: "2026 is the year of governance of the photovoltaic industry, and governance of the internal volume of the industry is the top priority."This statement marks that the regulation of disorderly competition in the photovoltaic industry has risen from the level of industry self-discipline to the strategic height of national overall planning.

with its performance advantages brought by extreme efficiency, clear cost reduction path, profound patents and prosperous ecological moat, rapidly expanding market application and strong guidance of national policies,

BC technology is no longer a "bonus item" on the icing on the cake, but a "necessary option" that determines whether enterprises can take the initiative in the new competition pattern and win the future ". When technology dividends replace capital expansion as the main engine of growth, and when high standards lead to replace low-cost roll-ins as the industry consensus, the rise of BC technology heralds the arrival of a new era of photovoltaic with efficiency and value at its core.