A consensus has long been established in the PV market: the best product does not necessarily prevail in the end, while the lowest-priced option often wins out. No matter how advanced a technology is or how well-conceived its concept, it will struggle to achieve long-term success if its price is too high or its operation is overly complex. Conversely, the lowest-priced product does not necessarily dominate the market. In the photovoltaic industry, the key to a product’s breakout success lies in striking the right balance among price, quality, and ease of use. After all, PV systems are designed and installed with a service life of over 20 years in mind. The manufacturer should have equipped the system with higher-quality materials and thicker glass. Additionally, the inverter and battery should have used more durable electronic components. However, the sustained decline in market prices has imposed tremendous pressure, constraining efforts to improve product quality. As a result, companies are forced to cut costs and optimize production processes at every stage, and even load more goods into each container to reduce shipping expenses. Often, whether a product lives up to its claims and whether cost-cutting has gone too far only becomes apparent after several years of actual use. As the year draws to a close, module prices have largely stabilized, suggesting that the market may have already hit bottom, with limited room for further price declines. Occasional price movements that deviate from the downtrend are usually driven by flash sales or inventory liquidations, rather than a shift in market structure. Given the substantial losses Asian manufacturers have incurred over many years, many in the industry expect module prices to eventually rebound. However, the timing and mechanism of this recovery remain uncertain. Higher prices could have given manufacturers the confidence to improve product quality again, but no tier-one suppliers are willing to be the first to raise their prices. Since mid-December, leading manufacturers such as LONGi and JinkoSolar have initiated price hikes in response to rising silver prices. N-type module prices have increased by RMB 0.03–0.05 per watt, bringing the adjusted quoted price to approximately RMB 0.75 per watt. According to Guojin Securities, module prices could rise to RMB 0.88–0.99 per watt by 2026.

Only diversified corporate groups that do not rely solely on the PV business, or small and medium-sized niche suppliers serving specific customer segments, have the confidence to set product prices above the industry-average market level reflected by the sector index. The failure of companies such as Meyer Burger and SunPower underscores that large-scale module production becomes unsustainable when manufacturing costs diverge sharply from current market prices. Despite possessing cutting-edge technologies like HJT, Meyer Burger was hampered by a high-cost production model. As a result, its 2024 sales nearly halved, ultimately plunging the company into a debt crisis and triggering delisting proceedings. This also presents a recurring challenge for system planners and procurement teams: the market is flooded with a wide array of products, yet reliable options are few and far between. Experience has shown that a conservative approach is usually more reliable when selecting components and system configurations. Innovation is indispensable in the photovoltaic industry and often leads to substantial increases in power generation; however, it also entails high risks. For capital-intensive, long-life assets such as photovoltaic power plants, component failures within just a few years of commissioning, or the disappearance of both the manufacturer and the warranty provider by the time issues arise, can lead to severe consequences.

There are quite a few such precedents. In the early 2010s, a shortage of semiconductor-grade polysilicon gave rise to photovoltaic-grade metallurgical silicon technology. Canadian Solar launched “E-modules” using this material; although competitively priced, they exhibited much faster degradation than conventional products, resulting in lower-than-expected power output. Ultimately, the company was forced to replace large batches of these modules, incurring substantial losses, and the technology quickly faded from the market.

There are also numerous ambitious R&D projects in the energy storage sector that have lost touch with the market. The now-bankrupt HPS company once developed the Picea household hydrogen storage system, which uses an electrolyzer to convert surplus photovoltaic power into hydrogen for storage. When electricity generation falls short, a fuel cell reconverts the hydrogen back into electricity and heat. However, its high cost has limited its appeal to only a small cohort of financially capable self-sufficiency enthusiasts. In contrast, electrochemical energy storage systems offer superior economics and, with proper configuration, can achieve near-complete energy self-sufficiency. Another company, Prolux Solutions, attempted to adapt mature flow battery technology from the utility-scale energy storage sector for residential applications. However, it underestimated the challenges associated with electrolyte circulation, resulting in leaks within just a few months of commercial deployment. Due to projected high maintenance costs, the company plans to recall or replace these systems with established lithium iron phosphate (LFP) battery storage technology by the end of 2025.

Some technological concepts require multiple rounds of R&D iteration or must await changes in the market environment before they can be fully developed and implemented; the integrated solar-thermal and photovoltaic collector is a prime example. This technology exhibits an inherent contradiction: excess heat reduces photovoltaic efficiency and necessitates continuous cooling; however, such cooling dissipates thermal energy, leaving insufficient heat to meet space-heating demands. Over the past two decades, numerous venture-capital-backed startups emerged to pursue this technology, yet all ultimately failed. A breakthrough was achieved only when R&D teams abandoned the costly back-side insulation design and integrated solar collectors with heat pumps capable of utilizing low-temperature thermal energy. To determine whether a new technology can achieve lasting market appeal, one practical indicator to consider is whether multiple companies are adopting similar technological approaches and bringing them to market. When multiple startups offering similar solutions successfully attract international venture capital, it often signals that the technology has long-term potential. Once such products achieve significant market penetration, the risk of failure drops substantially—at least until the next wave of disruptive technologies emerges.

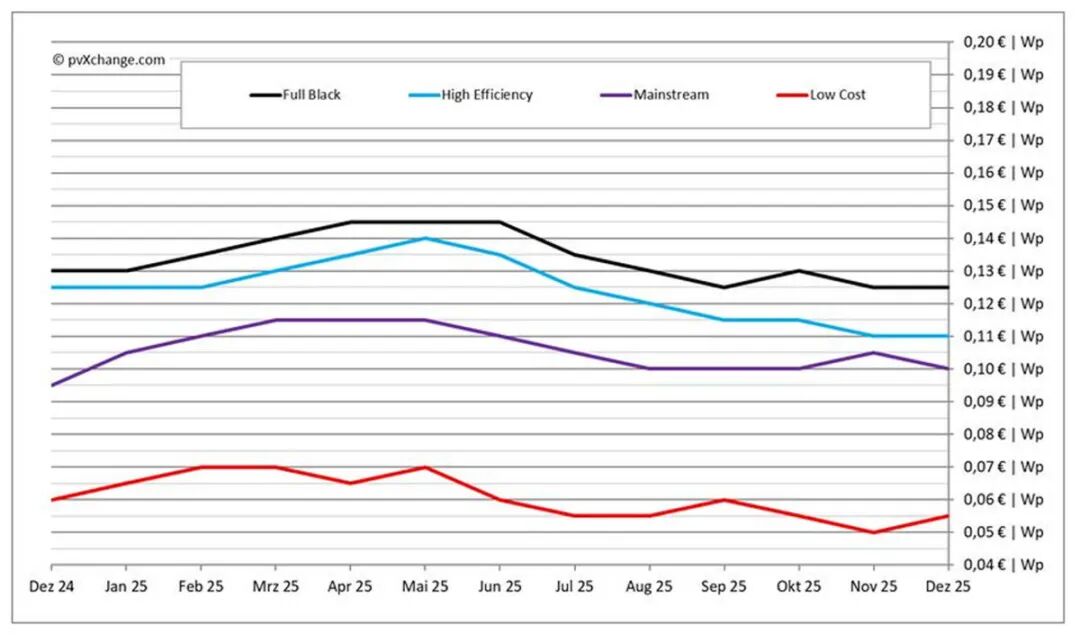

Overview of Photovoltaic Product Prices in December 2025 (including month-over-month changes; data as of December 15)