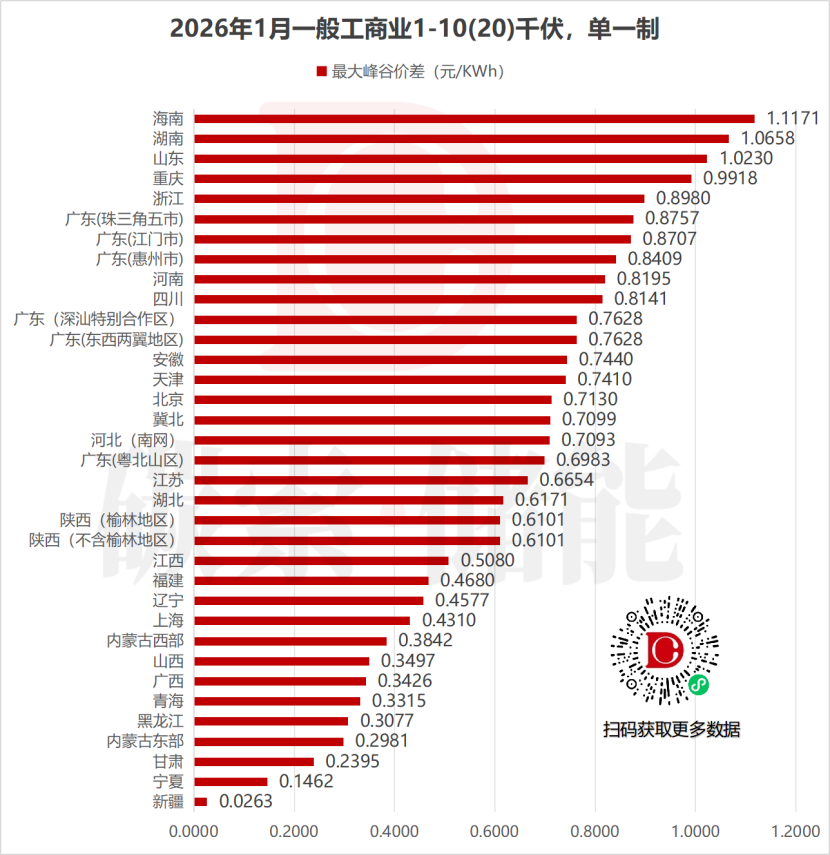

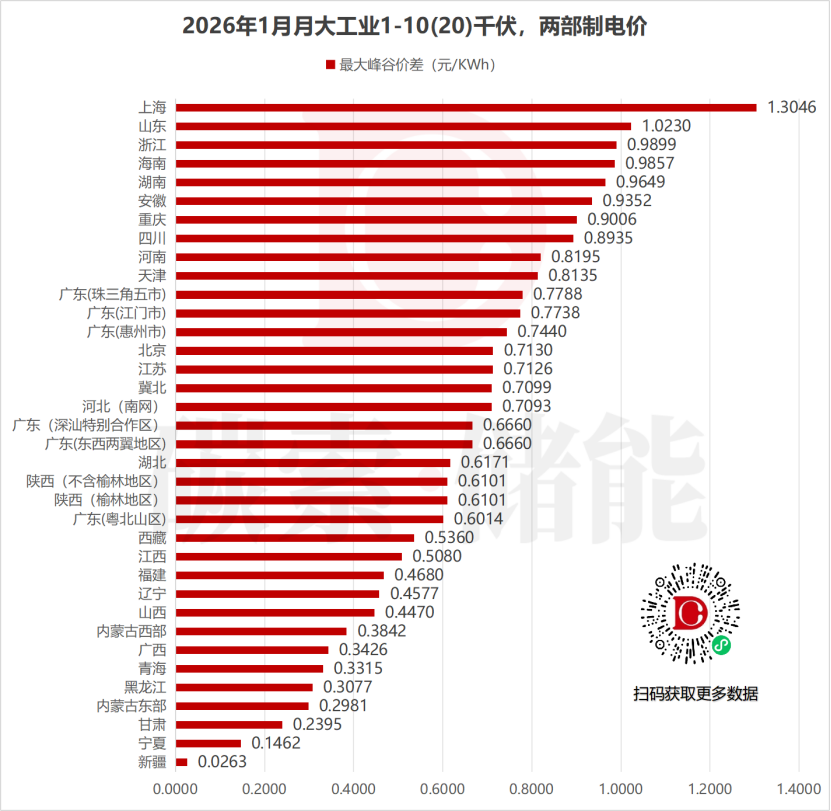

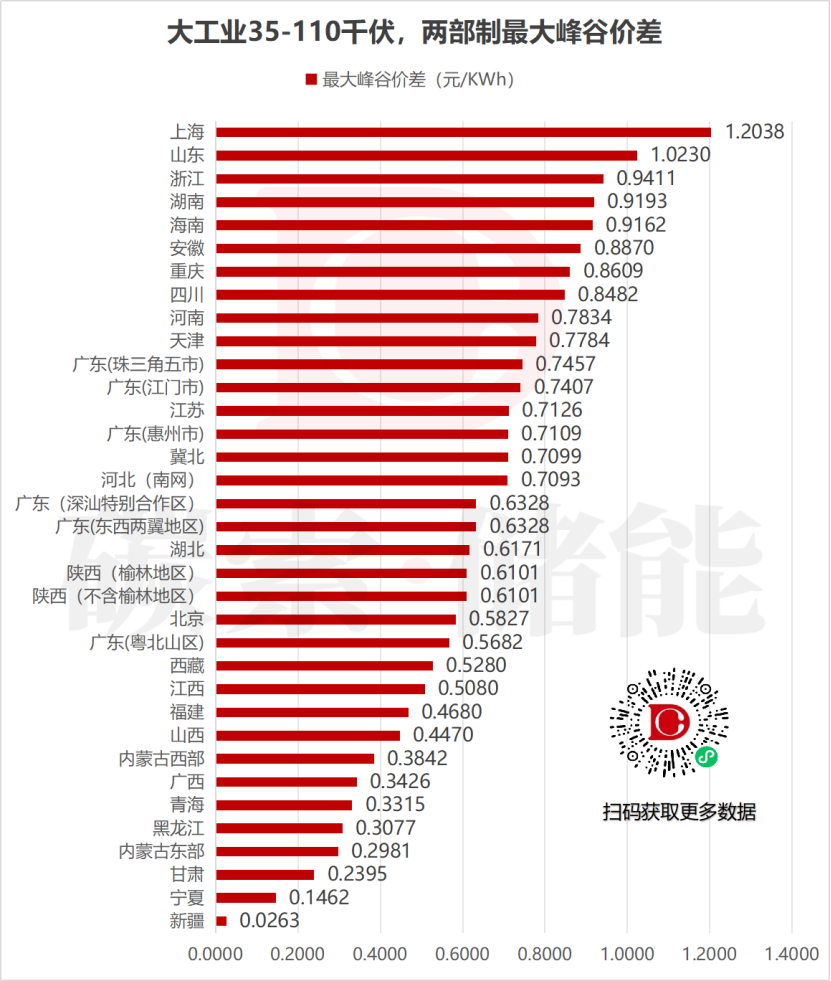

Four regions have retained valley-time electricity prices, while the peak-valley price differentials among regions have become markedly divergent. The peak–valley price spread has exceeded RMB 0.7 per kWh, with Hainan recording the highest at RMB 1.117 per kWh. In the large-industry sector, Shanghai leads in both the 1–20 kV and 35–110 kV voltage tiers, boasting a maximum peak–valley spread of over RMB 1.304 per kWh.

January remains the peak season for electric heating. In 21 regions across the country, a super-peak electricity pricing mechanism is being applied concurrently only to commercial and industrial users served by power procurement agents, with the aim of encouraging high-energy-consuming enterprises to shift their electricity usage to off-peak hours while also taking into account the operational needs of small, medium, and micro-sized businesses.

Anhui, Shanghai, and three other regions have specified that the super-peak electricity price will apply only to two-part tariff customers; single-part tariff customers will not be subject to it for the time being.

With regard to time-of-day pricing, Anhui has designated December 15 of each year through January 31 of the following year, with super-peak rates in effect from 19:00 to 21:00 daily. The super-peak rate is set 20% higher than the peak-hour rate. In northern Hebei, the super-peak period is limited to 17:00–19:00 daily throughout January, also with a 20% surcharge. Currently, direct-power-purchase customers in provinces such as Shaanxi and Liaoning have completely abolished the government-set fixed peak-period schedules and floating price ratios. Peak-hour prices are now determined through negotiations in medium- to long-term contracts or by supply-and-demand dynamics in the spot market.

Shandong: As a benchmark region for implementing deep-valley electricity prices, it will continue the 2025 time-of-use pricing policy in January 2026. The deep-valley period is set from 11:00 to 14:00, covering all commercial and industrial time-of-use customers served by power procurement agents.

Shanghai: Deep-valley pricing is limited to large-industry two-part tariff customers served by power procurement agents, further focusing on peak-shaving incentives for high-energy-consuming industrial users.

Anhui: Deep-valley pricing applies only to two-part tariff industrial customers served by power procurement agents and is implemented exclusively during public holidays, creating a dual-regulation mechanism of “strict peak-hour constraints plus precise low-demand incentives” alongside peak-hour pricing.

Notably, deep-valley pricing is generally tied to customers on the two-part tariff structure and targets high-energy-consuming users. Direct-market participants do not have a fixed deep-valley policy; their electricity prices are directly influenced by real-time supply-and-demand conditions.

Notably, the peak-to-valley price difference in Xinjiang is only RMB 0.0263 per kilowatt-hour, the lowest nationwide. This phenomenon fully demonstrates how the increasing share of new energy generation is profoundly reshaping electricity pricing mechanisms. According to data from State Grid Xinjiang Electric Power, at 14:45 on December 12, the output of new energy generation on the Xinjiang power grid surged to 40.17 million kilowatts, reaching a new all-time high. With renewable generation accounting for nearly 90% of total power output, the logic underlying the peak–valley price spread has undergone a fundamental shift, moving from being “peak-shaving cost–driven” to “new energy integration–driven.”

The Full-Abolition Model (Shaanxi, Liaoning): This model features a high proportion of direct-market participants. The government’s fixed time-of-use electricity pricing has been completely phased out, with retail electricity prices determined either by medium- to long-term 24-hour contracts or by the spot market. Peak and off-peak prices fluctuate dynamically in response to supply and demand. Partially liberalized model (Sichuan): Leveraging the hydroelectric generation profile that varies with wet and dry seasons, a fixed time-of-use tariff is maintained for proxy procurement customers during the flood season from July to August. For all other periods, customers are allowed to negotiate prices, thereby balancing renewable energy integration with grid stability. Reference Pricing Model (Jiangsu, Shandong): The catalog peak–valley prices are converted into reference prices. For power-purchasing-agency customers, the optimized time-of-use pricing remains in place. Direct-market participants may use the catalog prices as a reference for negotiation. This represents the mainstream transitional model nationwide.